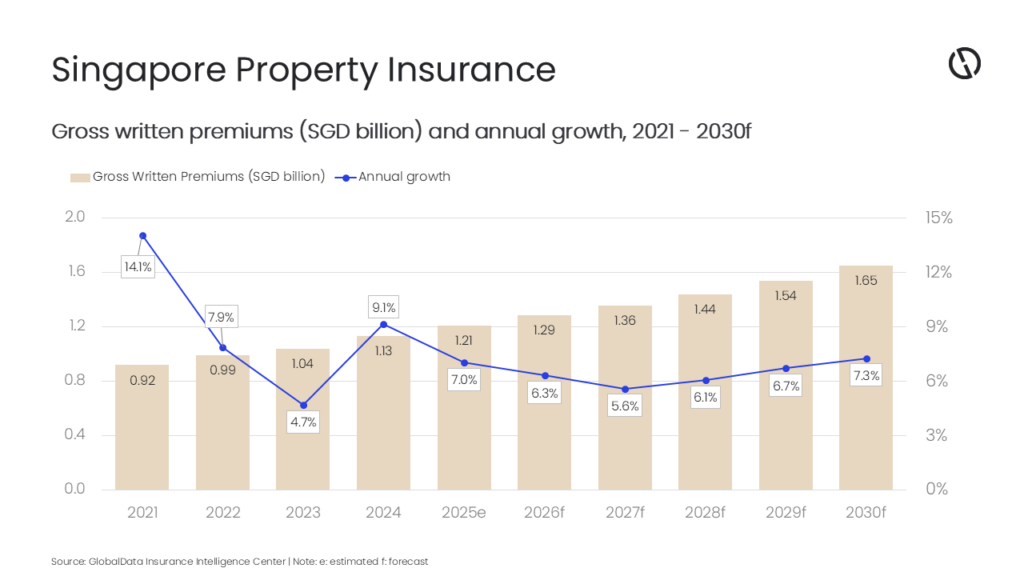

The property insurance industry in Singapore is projected to grow at a compound annual growth rate (CAGR) of 6.4%, with gross written premiums (GWP) increasing from SGD1.3 billion ($973.2 million) in 2026 to SGD1.6 billion ($1.2 billion) in 2030, forecasts GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the Singapore property insurance industry will register an annual growth rate of 6.3% in 2026, supported by the resilient property values and the ongoing development activity. This will be further supported by the infrastructure and housing projects, digital distribution, embedded insurance adoption, faster claims disbursement, and climate-resilient underwriting.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “The pipeline of new projects, rising residential values, sustained luxury demand, and investment in public infrastructure will continue to drive the growth of property insurance in Singapore.”

Housing and infrastructure activity will continue to support premium growth. Residential demand was buoyed by the rising Housing and Development Board (HDB) resale prices and upgraders with expectations for an increase in 2026, which will translate into higher sums insured and expanded coverage needs.

The luxury housing segment also strengthened with transactions valued at $5 million and above rising by over 20% in Q3 2025 compared to the same quarter in 2024, with average unit values nearing $10 million. This is a clear signal for higher-limit home policies and bespoke endorsements in the high-net-worth segment. Meanwhile, rents are set to climb through 2026 amid tight supply, supporting landlord-related covers and ancillary tenant solutions.

Regulatory recalibration will also shape property insurance dynamics in the near-term. The government has increased the holding period from three to four years and the seller stamp duty by four percentage points for each tier of the holding period in July 2025. Such changes will encourage long-term ownership and will increase the demand for comprehensive home insurance rather than short-term fire policies.

Sahoo adds:“Digital distribution and product innovation are accelerating property insurance sales in Singapore. The online insurance market is expected to grow further through 2026, with broader digitization enabling instant policy issuance, AI-enhanced underwriting, and seamless claims capabilities. This will benefit property insurers as they scale direct and partner-led channels. As insurers digitize, real-time payments infrastructure is enabling faster claims payouts after incidents, improving customer experience and trust, particularly following hazard events.”

Embedded insurance is gaining traction, with rising GWP as embedded distribution captures a growing share of property insurance. The premium-free home insurance, a complimentary built-in policy offered by rental platforms, for tenants covering contents, renovations, and selected incidents, is an example of how embedded products can close protection gaps in rental markets and support growth.

Risk awareness is rising alongside the evolving household exposures. Increase in residential fires is putting a spotlight on the limitations of mandatory HDB fire insurance (which covers structural reinstatement but not contents) and the need for optional home contents policies to avoid underinsurance. According to the Ministry of Home Affairs Singapore, the number of residential building fires has increased by 8.6% to 1,051 incidents in 2025.

Sahoo concludes: “Singapore’s property insurance market is on a durable growth path. Insurers that double down on embedded partnerships, digital distribution, and faster claims payouts, including real-time disbursements while integrating climate resilience into underwriting, will be best positioned to capture the premium growth and protect margins. With strong product innovation such as tenant solutions and niche in-home covers, supportive regulatory oversight, and rising risk awareness, the market is set to deliver sustained premium expansion through 2026–2030.”